By , SDR Ventures | June 28, 2016

Many owners are now considering selling their businesses as they approach retirement age. When considering their exit strategies, they face difficult decisions for monetizing the enterprise value of their businesses. While a business owner wants to receive a desirable price for the business, he or she may not want to sell to a third party (e.g., a strategic buyer or a private equity firm). The owner may instead want to reward loyal employees who have made significant contributions to the business’s success. If the owner is willing to receive fair market value vs. strategic market value, an Employee Stock Ownership Plan (ESOP) may be a practical exit strategy. Fair market value, which is based on the historical performance of a company, is typically less than strategic market value, which also takes into account future synergies.

Recently, SDR Ventures advised a client in a sales transaction in which the owner chose to execute an ESOP transaction versus other exit options available to him. Of utmost concern to this owner was rewarding his employees and keeping his legacy in-house.

How does an ESOP work? Below is a brief synopsis of this type of exit plan.

What Is an ESOP?

It is a type of qualified retirement plan similar to a profit-sharing plan, but with one main difference. An ESOP is required by statute to invest primarily in shares of stock of the ESOP sponsor (i.e., the corporation selling the stock). Unlike other qualified retirement plans, ESOPs are specifically permitted to finance the purchase of employer stock by borrowing from the corporation, other lending sources, or from the shareholders selling their stock.

When Congress authorized ESOPs in 1957 and defined their rules in 1974, it had two primary goals:

1) provide tax incentives for owners of privately held companies to sell their companies; and

2) provide ownership opportunities and retirement assets for working-class Americans.

How Does an ESOP Work?

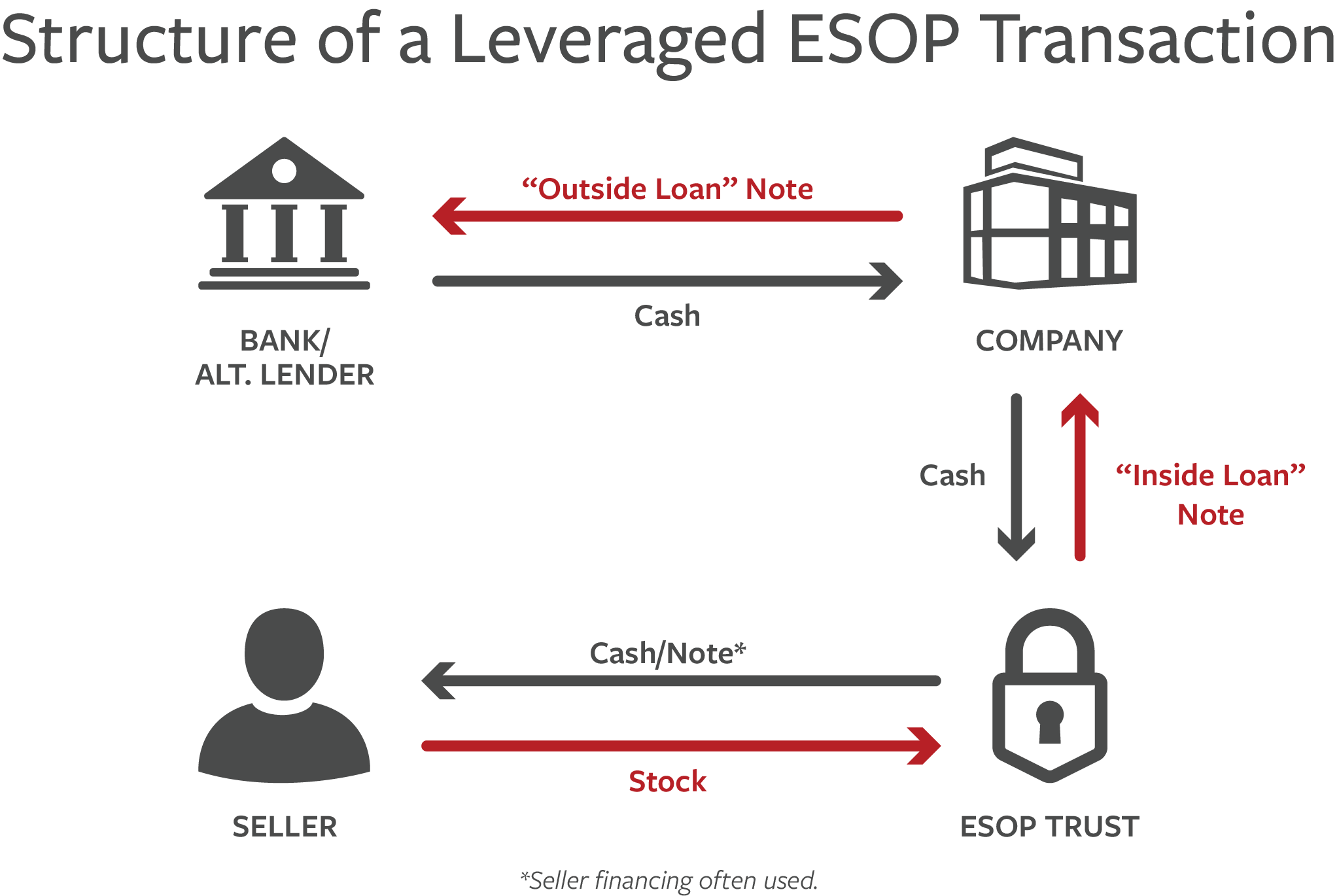

In a typical leveraged ESOP transaction, a corporation’s board of directors adopts an ESOP plan and trust and appoints an independent ESOP trustee. After obtaining an independent appraisal of the value of the corporation’s equity, the ESOP trustee negotiates the purchase of all or a portion of the corporation’s issued and outstanding stock from one or more selling shareholders. Often, the corporation sponsoring the ESOP will borrow a portion of the purchase price from an outside lender (the “outside loan”) and immediately loan the proceeds of the outside loan to the ESOP (the “inside Loan”) so that the ESOP can purchase the shares.

The two-phase loan process is used because lenders generally are unwilling to comply with restrictive ERISA loan requirements. If only a portion of the purchase price is funded with senior financing, the remaining portion of the purchase price generally will be funded through the issuance of subordinated promissory notes to the selling shareholders, whereby the sellers receive a rate of interest appropriate for subordinated debt.

To provide the ESOP the funds necessary to repay the “inside loan,” the corporation is required to make tax-deductible contributions to the ESOP each year, similar to contributions to a profit-sharing plan. Upon receipt of these annual contributions, the ESOP trustee uses the funds to make payments to the corporation on the “inside loan.” In addition to these contributions made to the ESOP by the corporation, the corporation can declare and issue tax-deductible dividends (C-corporation) or earnings distributions (S-corporation) on shares of the corporation’s stock held by the ESOP which, in addition to employer contribution, can be used by the ESOP trustee to pay down the “inside loan”. Shares purchased by the ESOP from selling shareholders (or the corporation) are held in a “suspense account” within the ESOP trust. As the ESOP trustee makes its annual principal and interest payment on the “inside loan,” shares of the corporation’s stock acquired by the ESOP from the selling shareholders (or corporation) are released from the suspense account and allocated to the separate ESOP accounts of employees participating in the ESOP.

Article LINK

For additional information regarding Florida business sales, acquisitions and valuations, please contact Eric J. Gall at Eric@EdisonAvenue.com or 239.738.6227. Also, visit our Edison Avenue website at www.EdisonAvenue.com or my personal website at www.BuySellFLbiz.com.

No comments:

Post a Comment